SMM October 11 News:

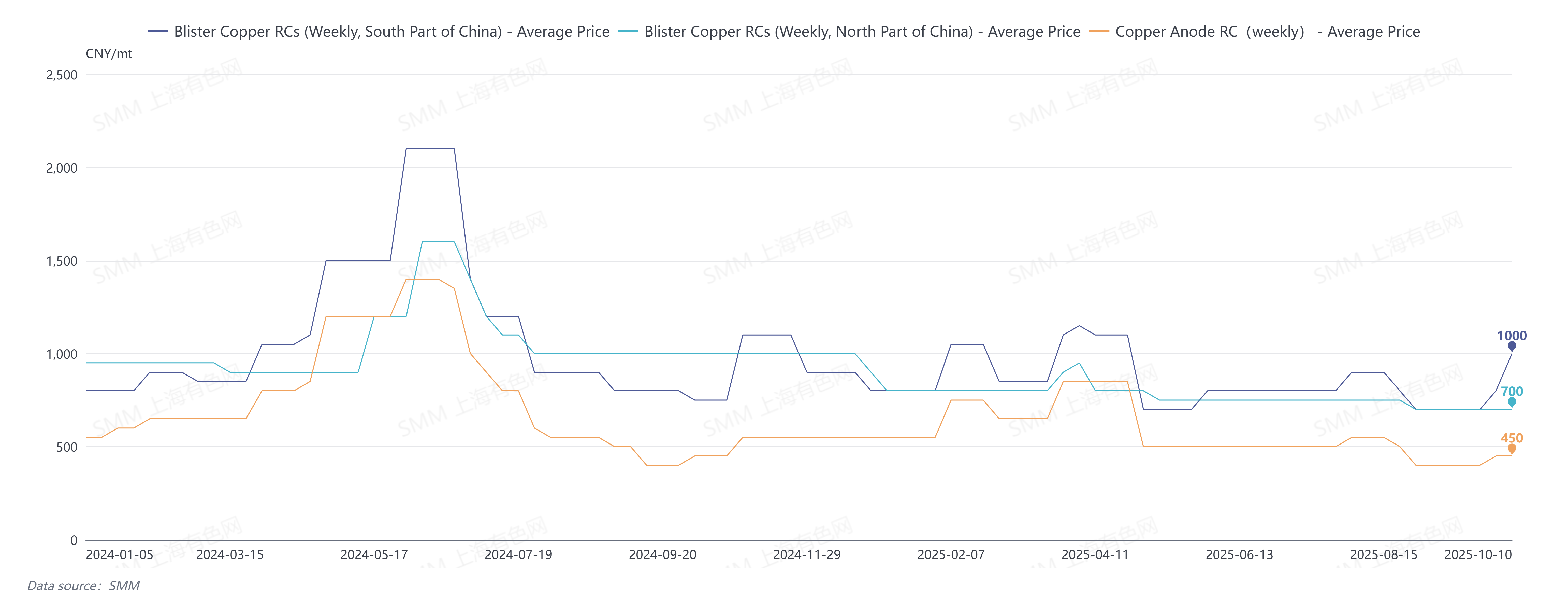

In September 2025, SMM quoted blister copper RCs in south China at 600-800 yuan/mt, averaging 700 yuan/mt, down 150 yuan/mt MoM; Blister copper RCs in north China were quoted at 600-800 yuan/mt, averaging 700 yuan/mt, down 50 yuan/mt MoM; Import blister copper RCs CIF China were quoted at 80-90 $/mt, averaging 85 $/mt, down 10 $/mt MoM.

The core contradiction in the blister copper market of China in September centered on "supply contraction and rising demand." Under the supply-demand mismatch, the overall market trended tighter, ultimately driving down blister copper RCs both domestically and overseas.

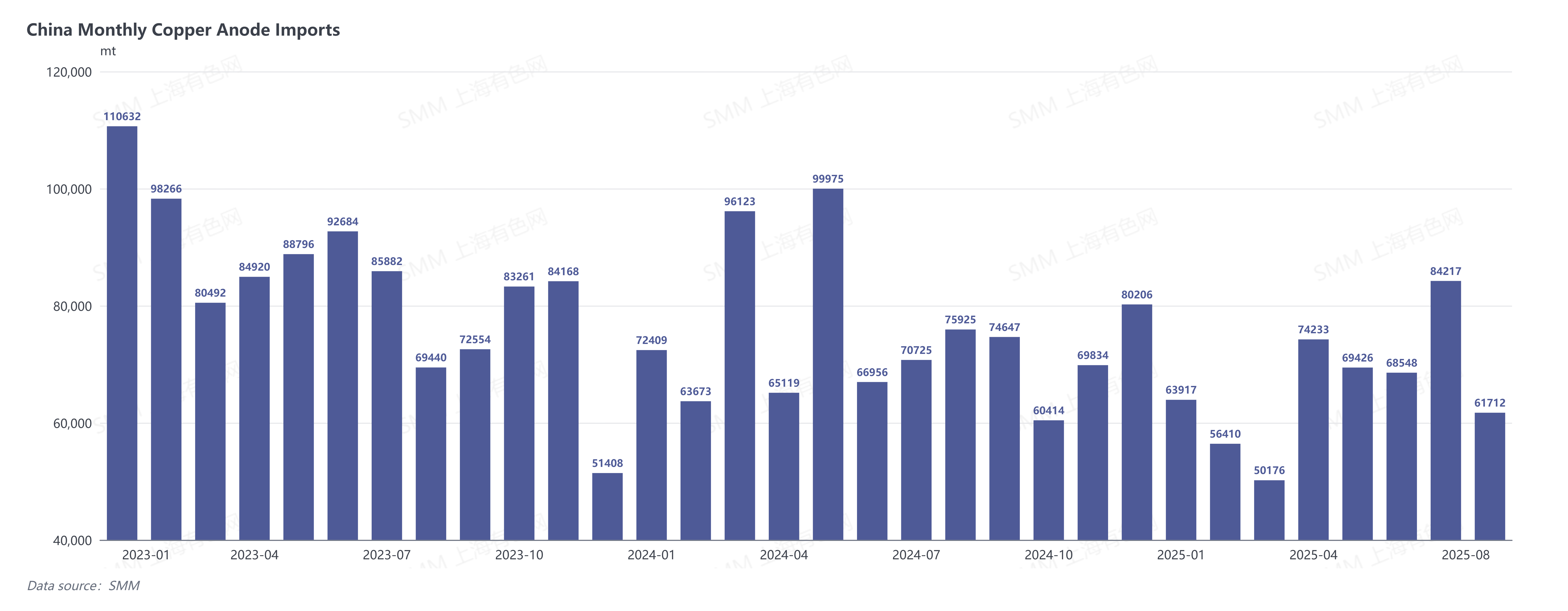

Supply side, uncertainty surrounding policies related to the secondary copper industry's standardization became a key constraint on market supply. Smelters in core regions such as Jiangxi and Anhui province, to avoid policy risks, opted to purchase only recycled copper raw materials with tax invoices. Some enterprises, facing unclear raw material costs and policy expectations, even chose to suspend production and adopt a wait-and-see approach. This directly led to a significant decrease in the supply of scrap-derived blister copper and anode plates. Meanwhile, China's imports of copper anode (HS code: 74020000) in August 2025 were 61,700 mt, down 26.72% MoM and 18.72% YoY; cumulative imports from January to August 2025 totaled 528,600 mt, down 13.47% YoY. The supply side overall showed a contraction trend.

Demand side, September to November marks the concentrated maintenance period for China's smelters. To minimize the impact on copper cathode production, market stockpiling demand for copper anode increased.

Entering October, the market holds expectations for improvement, but a complete reversal of the anticipated tightness is difficult.

On October 10, the SMM weekly blister copper RCs in south China were quoted at 800-1,200 yuan/mt, averaging 1,000 yuan/mt, up 200 yuan/mt WoW; weekly blister copper RCs in north China were quoted at 600-800 yuan/mt, averaging 700 yuan/mt, flat WoW; weekly import blister copper RCs CIF China were quoted at 90-100 $/mt, averaging 95 $/mt, flat WoW; copper anode processing fees were quoted at 350-450 yuan/mt, averaging 450 yuan/mt, flat WoW; import copper scrap ingot CIF China coefficients were quoted at 96.7-98.3%, down 0.3% WoW.

October's supply-side improvement was signaled mainly by the sharp upward shift in copper prices around the National Day holiday, which galvanized suppliers of recycled copper raw materials to release stocks, restoring supply of these materials and allowing some copper anode producers to close raw-material gaps, thereby underpinning stable production in October. Beyond this, the concrete implementation of policies affecting the secondary copper sector will remain the key variable driving future changes on the copper anode supply side.

Demand side, multiple overlapping factors will keep high-level demand for copper anode intact: first, the persistent copper concentrates supply deficit keeps TCs under pressure, prompting smelters—driven by cost and raw-material considerations—to increase substitution demand for copper anode; second, many smelters will still be in the blister-copper stage of maintenance from October to November, and to offset potential shortfalls in copper cathode output, the market will favor purchasing anode plates over blister copper.

Synthesizing changes on both supply and demand sides, the marginal recovery on the blister copper and copper anode supply side in October can ease some tightness, yet rigid support on the demand side persists. The overall tight supply-demand balance is unlikely to reverse fundamentally; only blister copper RCs in China are expected to rebound, and the increase will be limited.